Practical Money: The Best FREE Credit Cards For 2026 Returning 3-6%

Getting the most from your credit cards.

Introduction

As the kids say, it’s been a minute. My apologies for the long gap between newsletters; things have been busy on this end. But life is calming down as spring approaches, which means two things: better weather and more time for me to obsess over credit card reward structures. I plan to grace your inbox at least twice a month until I get distracted by a shiny new high-yield savings account.

Back in 2024, I posted my favorite credit cards of that year with a minimum of 2% cashback. 2% is now officially chump change. We’ve leveled up. If you aren't getting at least 3%, are you even trying to win at capitalism?

One card that has been unceremoniously yeeted off this list: SoFi. In February, they started charging a monthly fee to many users. Some people still get the card with no fee, but I’m fairly certain I was selected for the fee because I committed the unforgivable crime of paying my balance in full every month. I closed the account faster than a SoFi stock price drop and found better options.

Also, in one of the first issues of this newsletter, I discussed how much I hate credit card debt. It is the financial equivalent of a “Kick Me” sign. In that newsletter, I discussed how I got out of debt coming out of college, as well as other strategies to get out of credit card debt, which you can read here.

Below are the credit cards I use regularly that offer at least 3% cashback, up to 5%, with no annual fee… well, technically, the Robinhood Gold Card sorta has a fee, but we’ll get to that in a minute. Nothing in life is free, except unsolicited financial advice on the internet. These are everyday cards; I’ll do a separate newsletter with credit cards we use for travel at some point.

Below those, I also list some other popular no-fee credit cards that I am currently not personally using. However, there is one that has 6% cash back in the category of your choice that I stumbled upon while doing my research for this newsletter, which immediately caught my attention because I am genetically incapable of ignoring free money. I plan to sign up for that one this week.

Oh, and I’m not paid by any of these companies. No referral kickbacks, no affiliate drama. If I ever do get sponsored, you’ll know because I’ll suddenly sound unnaturally enthusiastic. However, if you find this newsletter useful, please share it using the button below so I can continue yelling about credit cards on the internet:

A quick reminder, because the lawyers told me to: this is not financial advice. I am not a fiduciary, a CPA, or even particularly good at assembling IKEA furniture. This is just me sharing my strategies, investments, stocks, index fund strategies, what I’m buying, and where I plan to take those investments. Everyone’s financial goals are different—some of you want a yacht, others just want to stop looking at your 401(k) statements. No financial decisions should be made solely on this newsletter, which is for informational and entertainment purposes only and is not a substitute for advice from a qualified professional who actually knows your situation and charges by the hour.

First Steps When I Get A Credit Card

I don’t carry credit card debt. Every card I have is set to automatically pay the full balance each month, which means I never pay interest. Credit card companies hate this one simple trick. If having a credit card makes you more inclined to splurge on avocado toast or artisanal soap, just stick to cash or a debit card, my friend. The rewards are pointless if they cause you to overspend.

The first thing I do when I get a new credit card is set up autopay for the full balance. This removes the possibility of accidentally paying interest, which is how credit card companies actually make their money.

Another thing I do is maintain a Google Doc listing the benefits of every credit card I own. This sounds obsessive because it absolutely is. But many cards offer useful perks—rental car insurance, travel protections, purchase protection, foreign transaction fee waivers, etc. After you accumulate a dozen cards, it becomes impossible to remember which one does what.

The document keeps everything in one place, so I don’t have to spend 10 minutes Googling whether a card covers rental car insurance while standing awkwardly at the Hertz counter.

General Credit Cards I Use

Below are the credit cards I use regularly, and the reason for each. With these, I receive 3-5% cashback or rewards that I wouldn’t have received if I had used checks or a credit card.

Between the cards listed below, my store cards, and my travel cards, I have about 12 credit cards. Before you call a financial intervention, I should clarify that I only carry two cards in my wallet: the Robinhood Gold Card and the Capital One Savor card. The rest are either stored in my Apple Wallet or are in my desk drawer for whenever I need to actually use them, like when I purchase airline tickets or hotel reservations.

Alright, enough buildup. Here’s the list, starting from the bottom.

Robinhood Gold Card (3% cash back on everything)

This shiny new addition is one of the two credit cards I actually carry in my wallet. We use this for everything else when the cards below aren’t appropriate. There is no annual fee, no international transaction fees, and you get 3% cash back on everything (with a catch, more on that later).

There are some cool features with this credit card, like there is no credit card number on the physical card. It’s a mystery rectangle. If I lose it, I don’t have to update my 47 automatic payments because the “virtual” number in the app stays the same.

Also, you can create virtual cards in the app, which are basically new credit cards for whatever you want. You can create them for a one-time purchase or as an alternative credit card. For instance, I have a virtual credit card for my automatic payments, so if my regular card number from the app ever got compromised, I don’t have to spend an afternoon updating payment info across half the internet. We use this virtual card for our gym memberships, cell phone bills, insurance, our daughters’ dance classes, etc.

Now to the caveats:

To be eligible for the credit card, you have to be a Robinhood Gold member, which is $5 / month or $50 annually. I have a Robinhood Gold membership because it includes a 3% IRA contribution match, 3.35% APY in their brokerage account, and several other perks. Since our IRAs are already with Robinhood, the IRA match alone easily covers the membership cost.

Important: To receive the full 3% cashback, you must redeem points into a Robinhood brokerage account. If you apply the points directly to your credit card balance, the redemption value drops to 0.7 cents per point. In other words, if you do the normal thing people expect to do with credit card points—pay your bill—you get 2.1% cashback instead of 3%. Don’t be lazy. Move the money.

There is a waitlist. It took months to get. It’s more exclusive than a nightclub I’d never be allowed into.

There is no customer support phone number. If you need help, you go through the app. If a phone call is required, you request one. In other words, the relationship is a bit like texting a teenager.

If this sounds like a good fit, you can get more details and join the waitlist at this link.

Capital One Savor Rewards (3% back on dining, grocery stores, entertainment, and streaming services).

This is our dining card. When we signed up, the card offered 4% cashback on dining and streaming, and we were grandfathered into that rate. Which means we will cling to this card until Capital One pries it from our cold, financially responsible hands.

For new customers, the card now offers 3% cashback on dining, grocery stores, and popular streaming services with no annual fee (our card has a $95 annual fee). If you have the Robinhood Gold card, you probably don’t need this since the Robinhood Gold card gives you 3% cash back on everything anyway. The card excludes superstores like Walmart and Target. Streaming services that qualify include things like Netflix, Hulu, Disney+, etc.

The card also has no foreign transaction fees, so we use it for dining when traveling internationally as well.

You can get more information about this card by clicking here.

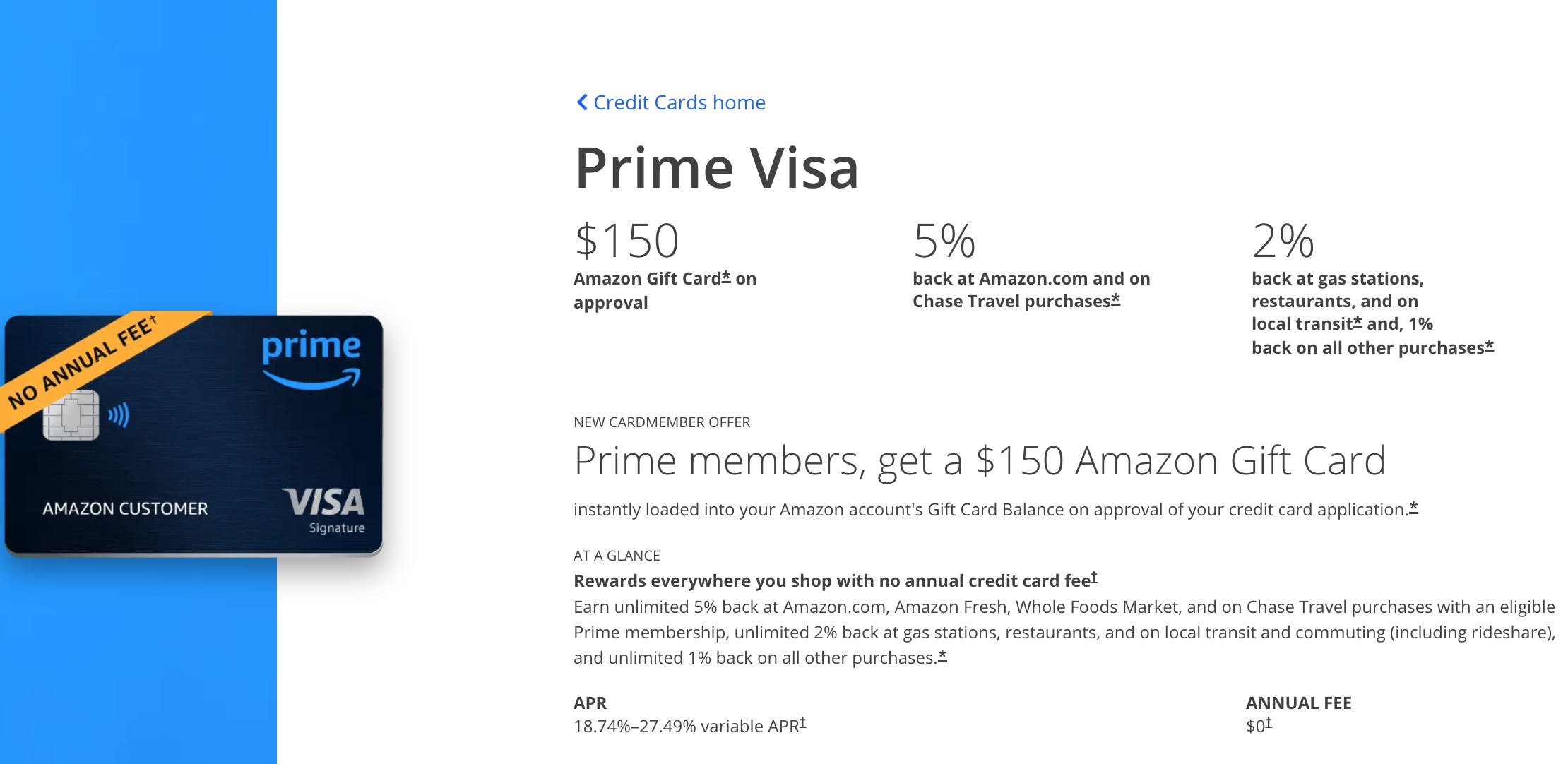

Amazon Prime Card

This one gets a lot of usage. I have two daughters, which means Amazon packages appear at our house with the regularity of mail delivery. Also, my wife thinks Whole Foods is a second home, which is great for nutrition and terrible for wallets. Thankfully this card gives 5% cashback on Amazon and Whole Foods, which softens the financial blow slightly. You also receive 5% cash back on Chase Travel purchases.

We’ve got this card saved in our Amazon account, and it’s on my Apple Watch for quick access at Whole Foods—because nothing says “modern parent” like paying for groceries with a smartwatch.

You can get more information at this link. New Prime members currently also receive a $150 Amazon Gift Card if they sign up and are approved.

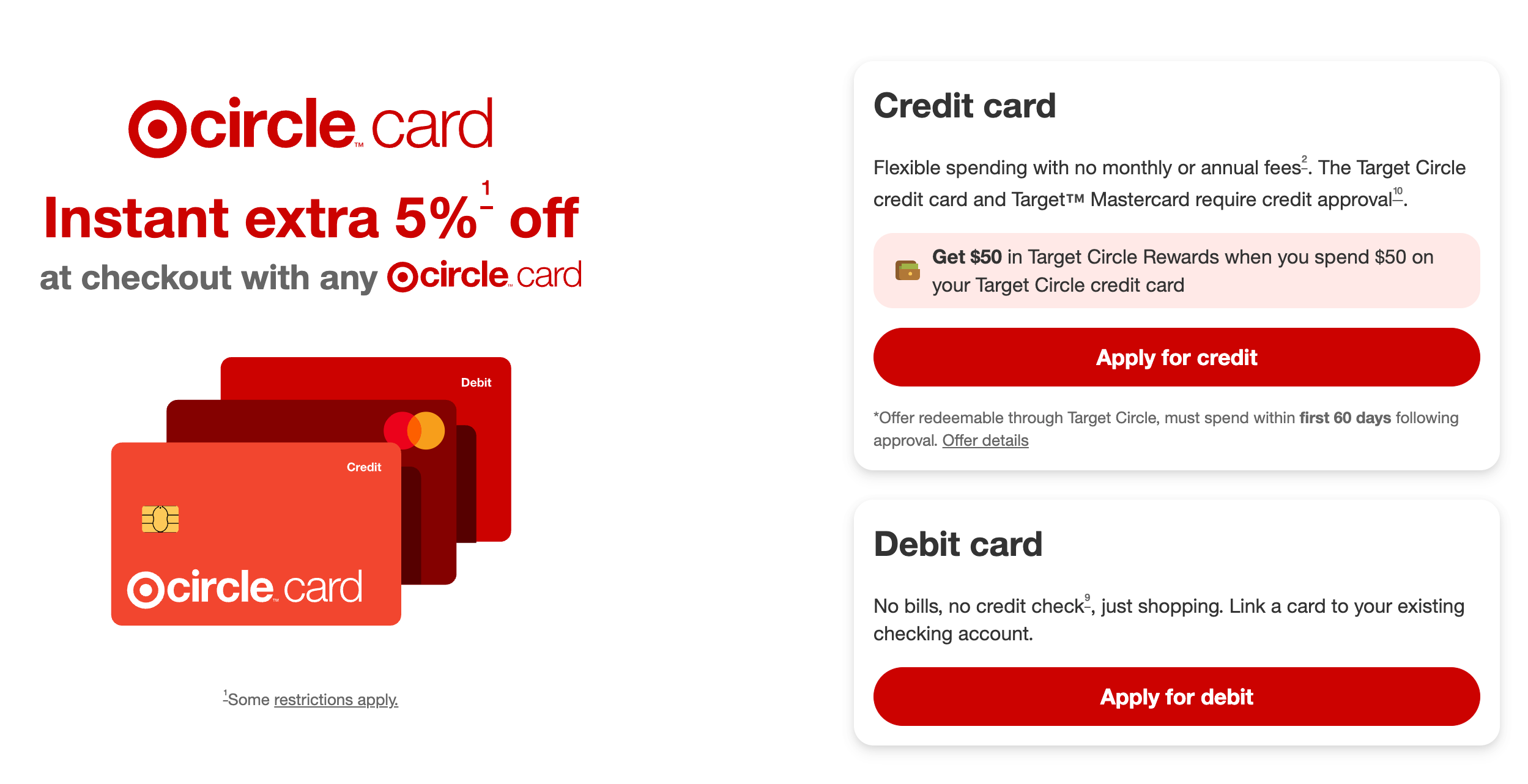

Target RedCard (5% back for purchases at Target & Target.com)

For everyday items that we don’t buy at Amazon, we shop at Target. Our daughters are also Target enthusiasts, which is the polite way of saying they somehow enter the store for toothpaste and leave with candles, throw pillows, seasonal decorations, three items you didn’t know existed, and somehow still forgot the toothpaste.

The Target RedCard gives 5% off all purchases at Target and Target.com. More details are available here. New members receive $50 in Target Circle rewards when they spend $50 on the card.

Honorable Mentions

These are cards we still have but rarely use.Think of them as the bench players of our credit card lineup.

Fidelity Rewards Visa Signature Credit Card (2% - 3% on everything)

This is our backup card, so if there is ever an issue with our Robinhood Gold Card, we use this instead. With the type of Fidelity account we have, we receive 2.25% cash back. With the rewards from this card, you can deposit them into any eligible Fidelity account. We have the cash back automatically deposited into our Fidelity Cash Management Account every month.

You can get more information about this card here.

Citi Double Cash Card (2% cash back on everything, our fallback card).

The OG 2% card, now sitting quietly in our drawer. Still fine, just outclassed. It earns 1% when you spend, 1% when you pay, and 0% excitement overall.

With 2% cash back, it is the worst-performing of the cards mentioned so far. It also has a 3% foreign transaction fee, and foreign currency purchases do not count for rewards, so don't take it to Paris unless you want to be insulted by the waiter and your bank.

You can get more details on this card here. New members earn $200 cash back as points after spending $1,500 on purchases in the first 6 months of account opening. The points can then be redeemed for $200 cash back.

Other Cards

Below are two other popular credit cards with no annual fees; we do not personally own any of them, although I will be signing up for the Bank of America Customized Cash Rewards card.

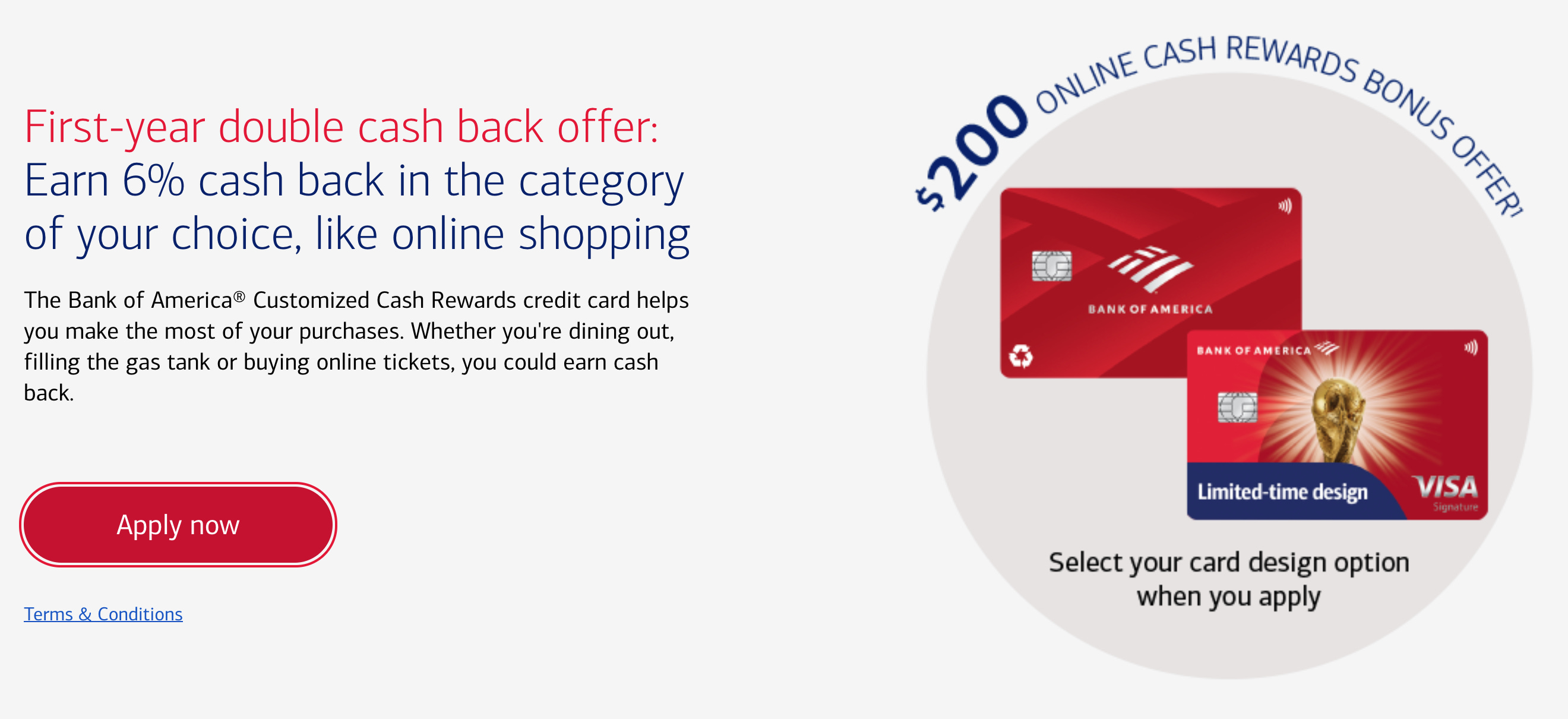

Bank of America Customized Cash Rewards (6% cash back in a category of your choice for one year)

I discovered this card while researching this newsletter and immediately thought: Well that seems suspiciously generous. I just stumbled upon this card while doing research for this newsletter, and I plan to sign up for it this week. You earn 6% cashback in a category of your choice during the first year, up to $2,500 per quarter in purchases. After the first year it drops to 3%, which is still solid. You also get 2% cash back at grocery stores and wholesale clubs, and 1% cash back on all other purchases. They are also offering a $200 online cash rewards bonus after making at least $1,000 in purchases in the first 90 days of your account opening.

We spend a lot on dining out, but I plan to use this card for the first $2500 each quarter, then switch back to the Savor card once that cap is reached. You can learn more about this card here.

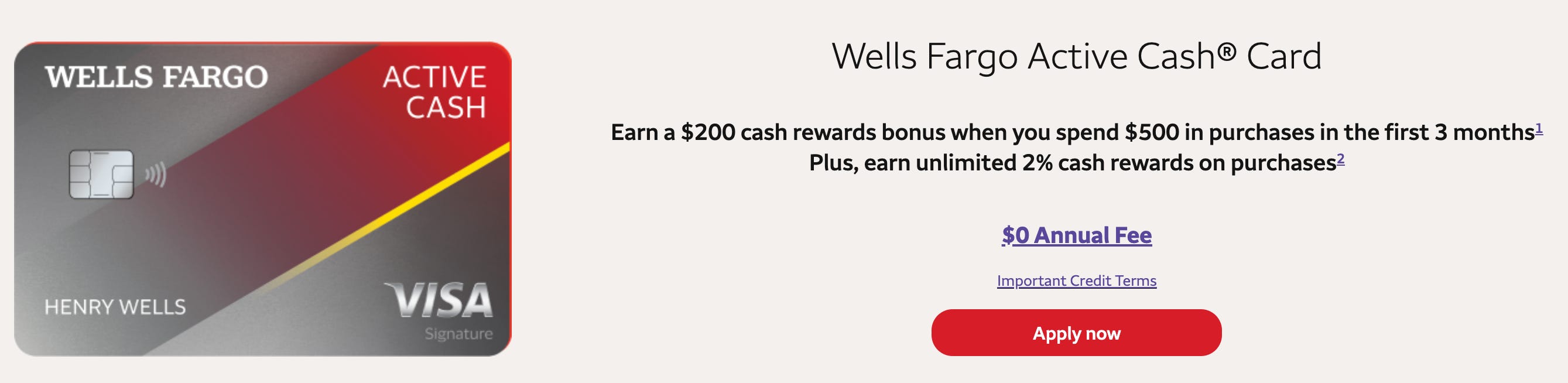

Wells Fargo Active Cash Card

Another popular card with no annual fee where you earn unlimited 2% cash rewards on purchases. New customers also get a $200 cash rewards bonus when they spend $500 in purchases in the first 3 months. It’s simple, reliable, and requires almost zero thinking… which honestly describes most of the financial products people should use. You can get more details at this link.

Conclusion

That’s the lineup. The secret to credit card rewards is simple: Pay the balance in full, collect the cashback, and let the banks wonder why you’re not paying interest as they planned. Always remember: If you carry a balance, you lose. Because while 5% back is nice, paying 25% in interest is not. If you carry a balance, the cashback you earn just becomes a very complicated coupon.

That's it for this week! As always, no financial decisions should be made solely on this newsletter, which is for informational and entertainment purposes only and is not intended to be a substitute for advice from a professional financial advisor or qualified expert. If you haven’t already, please subscribe to this newsletter below and never miss an update: