Super-Charging Your Fixed Income With ETFs

Make the most out of your cash

Introduction

If you’ve been reading this newsletter for a while and you’re not earning at least 3% on your cash, then we need to have a talk. Not an angry talk—more like a disappointed financial dad talk. Because at that point, it’s not the market failing you… it’s you ignoring me. Even though the "easy" money from high-interest savings accounts is beginning to evaporate as the Federal Reserve continues its suspenseful, extremely dramatic, slow-motion pivot—eyeing a target range of 3.0% to 3.5%, there are other alternatives to make the most out of your cash.

Whether it’s the loose change sitting in my checking account or my emergency fund in savings, every dollar I have is at least earning a minimum of 3.5%.

In this newsletter, I’ll go over my simple fixed income investments, from boring-but-beautiful cash options to slightly spicier plays like CLO ETFs that actually pay you for your patience.

A quick reminder, because the lawyers told me to: this is not financial advice. I am not a fiduciary, a CPA, or even particularly good at assembling IKEA furniture. This is just me sharing my strategies, investments, stocks, index fund strategies, what I'm buying, and where I plan to take those investments. Everyone’s financial goals are different—some of you want a yacht, others just want to stop looking at your 401(k) statements. No financial decisions should be made solely on this newsletter, which is for informational and entertainment purposes only and is not a substitute for advice from a qualified professional who actually knows your situation and charges by the hour.

Also, if you find this newsletter helpful, please share it with one friend who might find it useful by using the button below.

Checking / Cash Management Accounts

Ah yes, the checking account—where your money goes to earn absolutely nothing… unless you’ve evolved.

I’ve mentioned this before, but our default “checking account” is technically not a checking account, but it works almost exactly like one, minus the stale lollipops and the judgmental silence of a physical branch.

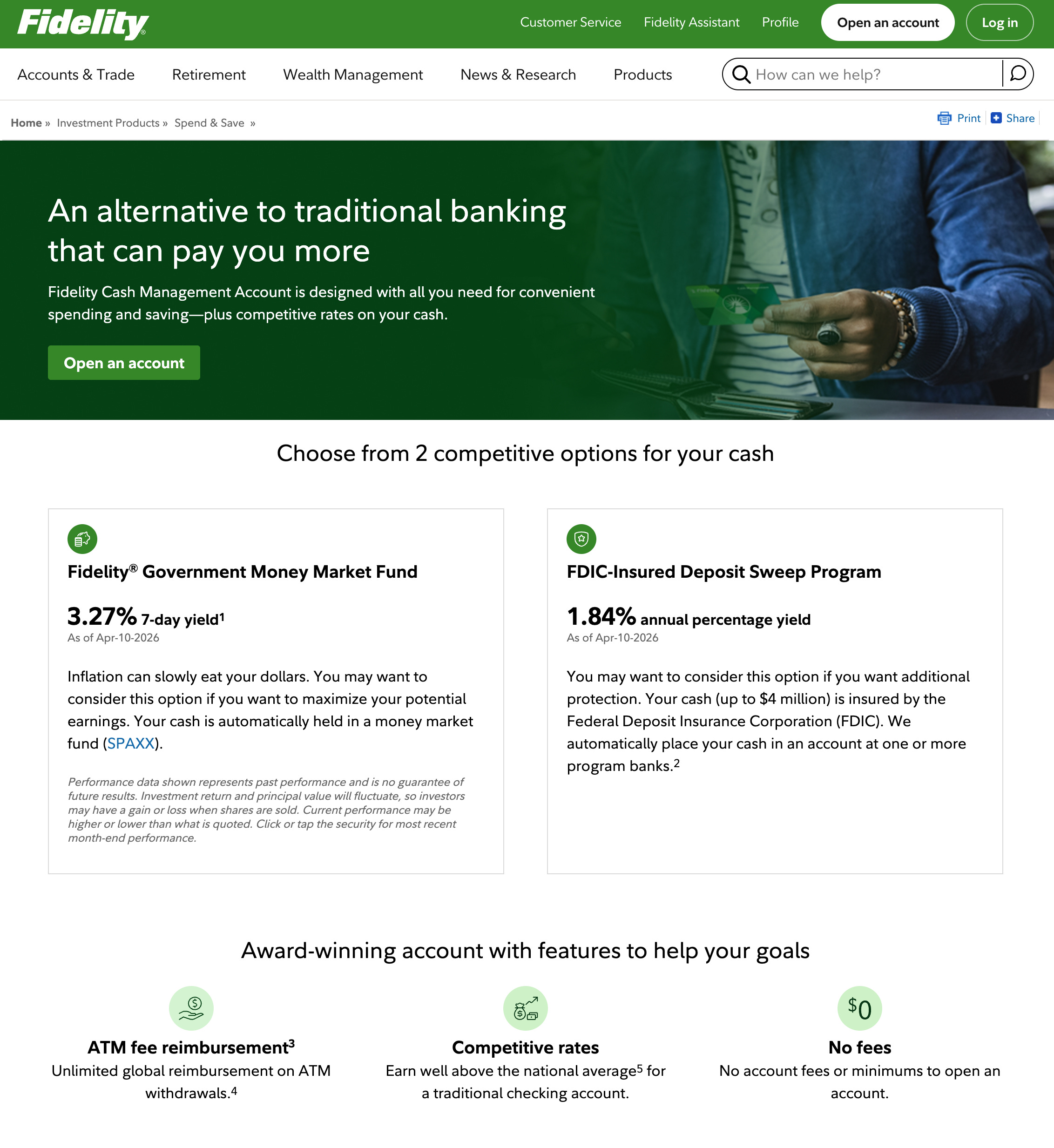

We use the Fidelity Cash Management Account, which has features similar to those of a traditional checking account, including the ability to write checks, make deposits, use a debit card, and access ATM withdrawals (with fees reimbursed, because paying to access your own money is a scam). We deposit all of our checks using their app, and really don’t have any need to go into a branch.

Best of all, you can choose to have your cash parked in the Fidelity Government Money Market Fund (SPAXX), which, as of this writing, has a 3.27% yield… 32,600% higher than the 0.01% yield we received with our old Chase checking account. Or you can have your cash in their FDIC-Insured Deposit Sweep Program, which offers a lower 1.84% annual percentage yield; it still trumps the Chase checking account yield by 18,300%. You can check out my 2024 newsletter about this account and learn how you can earn an even higher yield by using a different money market account like FZDXX.

However, it is a brokerage account and not a bank account. There are things you can’t do that you can with a regular bank, like depositing cash, opening a safe deposit box, getting documents notarized, exchanging foreign currency, etc. If you need services like that, you can use a branch account in conjunction with a Fidelity Cash Management Account.

Some alternatives to the Fidelity Cash Management account include:

Robinhood Checking (3.5% APY): We use this for our rental properties. You receive a 3.5% APY with a direct deposit of at least $1000 / month.

Vanguard Cash Plus (3.1%): New customers receive a 0.25% boost effective through September 30, 2026, which raises the APY to 3.35%. There is a $25 annual fee that is waived if you sign up for e-delivery.

HYSA (High-Yield Savings Accounts)

This is the boring-but-essential bucket, a place where you can keep an emergency fund that contains 3-6 months of essential living expenses. It’s the financial equivalent of a fire extinguisher-you hope you never need it, but when you do, you really do. I also use this account for taxes, and my quarterly estimated tax payments are made automatically from this account.

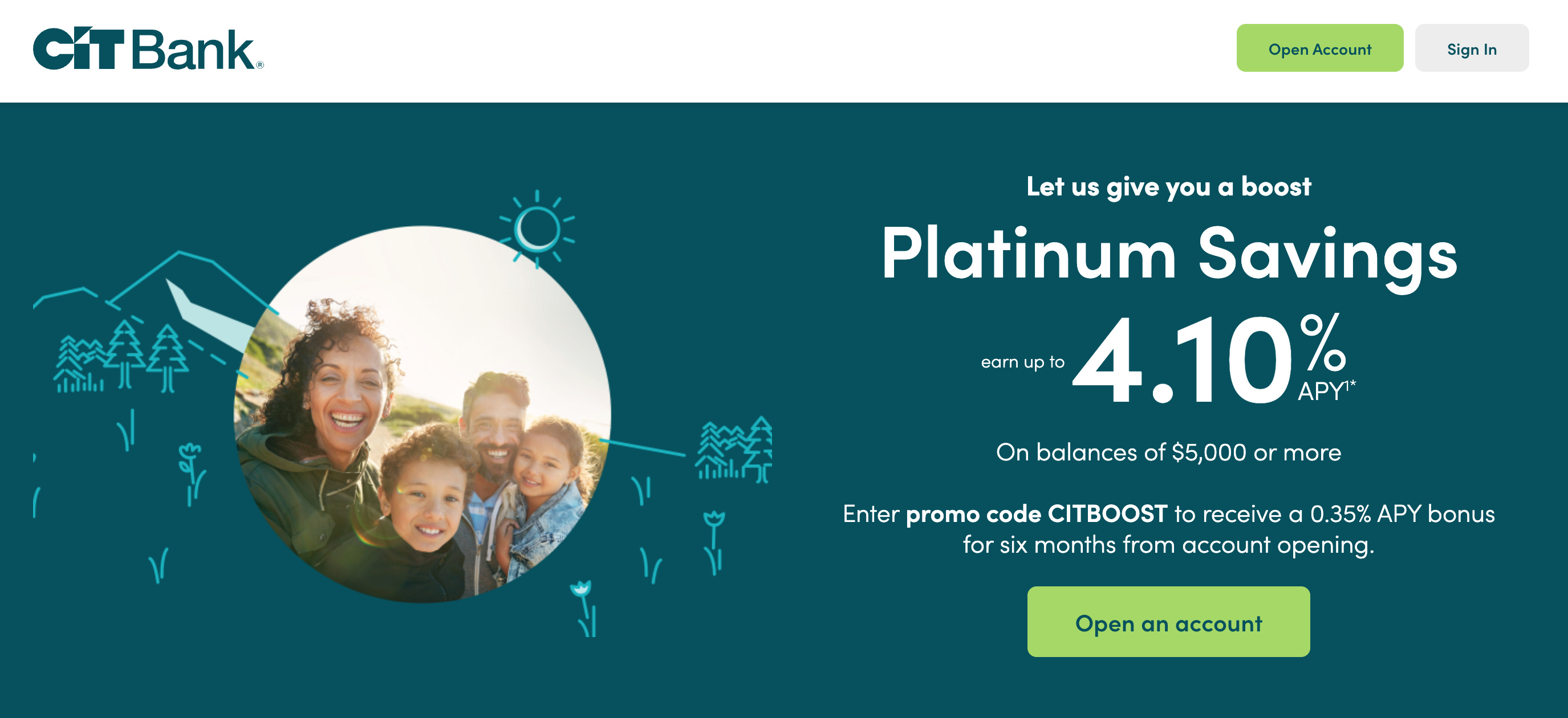

I wrote an article listing my favorite HYSAs back in 2023 here. CIT Savings remains our main HYSA with a 3.75% APY on balances of $5,000 or more (they are currently offering a six-month 0.35% boost for new customers for six months, bringing the APY to 4.10%).

Some other alternatives include:

Sofi Savings (3.3%): I’ve used this account in the past, and it was solid. For a limited time, they are offering a 0.70% boost for new customers, bringing the yield up to 4%.

AMEX High-Yield Savings Account (3.2%): Another account we’ve had in the past. This is a good option if you’re looking for more of a brand name.

Lending Club (3-4%): You earn a rate of 4% APY by depositing $250+ per month. Months without the deposit receive a 3% APY.

Money Market Funds

Money market funds (MMFs) are like HYSAs that went to business school. They are often used by investors with larger balances or brokerage accounts. MMFs often yield slightly more than HYSAs, though they carry a sliver more risk as they are not FDIC-insured (though they aim for a stable $1.00 NAV).

I use Money Market Funds to park cash in my stock and ETF investment accounts. It’s a good place for idle cash that I may deploy later, but which doesn’t need to sit around earning nothing while it waits for me to make a decision.

Some MMFs I’ve invested in include:

Fidelity Money Market Fund Premium Class (FZDXX) - 7-day yield of 3.44%; there is a $100,000 minimum to invest. An alternative with no minimum to invest is the Fidelity Government Money Market Fund (SPAXX), which has a 3.29% 7-day yield.

Schwab Value Advantage Money Fund (SWVXX): 7‑day yield of about 3.46% with no minimum to invest.

Vanguard Federal Money Market Fund (VMFXX): 7‑day yield of roughly 3.56% with a minimum investment of $3000. While it has the best yield of these three listed, its tech is archaic, and the customer support lags far behind Fidelity and Charles Schwab.

Treasuries, Agency Bonds, Corporates and CDs

This is where things start sounding like a CFA exam. I ladder these for a steady monthly income—because nothing says “I’ve matured financially” like getting excited about bond ladders. I broke down my fixed-income portfolio of treasuries, agency bonds, and CDs back in September of 2024, as well as how I ladder them for monthly income; you can read that here.

Treasuries remain one of the core building blocks of fixed income because they are backed by the U.S. government. Short-term Treasury bills are often used for cash management, while longer-duration Treasuries can offer more yield if you are comfortable with interest-rate risk.

Certificates of deposit, or CDs, are another straightforward choice for investors who want a known rate and maturity date. Bank CDs can be attractive when you want to lock in a rate and don't mind your money being "in jail" for a few months.

Agency bonds are issued by government-related entities such as Fannie Mae, Freddie Mac, and other agencies. They usually offer a bit more yield than Treasuries, though the exact tradeoff depends on the issuer, maturity, and structure. Think “Treasuries with a personality.”

Corporate bonds are issued by corporations; they represent debt obligations of these entities. These bonds typically offer higher yields than government or agency bonds due to their increased risk profile because companies can, in fact, mess things up.

A simple way to think about the three is this: Treasuries for safety and simplicity, agency and corporate bonds for a modest yield pickup, and CDs for rate certainty if you can lock up the money.

I took a deeper dive into agency and corporate bonds in 2024; you can read that issue here.

My Leftover Cash: SGOV and CLO ETFs

As noted, I use high-yield savings accounts for cash set aside for emergencies and taxes. I use Money Market Funds for cash in my investment accounts that I plan to use for stocks, ETFs, and options.

For the rest of my cash, I invest it in two vehicles: SGOV and JAAA. About 30% is in SGOV, with the other 70% in JAAA. Here’s a breakdown of the two.

SGOV

The iShares 0-3 Month Treasury Bond ETF (SGOV) is basically Treasuries with a gym membership—lean, efficient, and easy to trade. It holds 0–3 month U.S. Treasury bills, which are about as close to “boring and safe” as the market gets. You get yields that are close to Treasuries without managing individual bonds. The fund’s price barely moves, and it distributes income monthly. It’s what you buy when you want your money to do something… but not too much.

SGOV has grown into a massive vehicle, with over $84 billion in assets under management. Its 30-day SEC yield currently sits at 3.6%, while individual 0-3 month U.S. Treasury bills are hovering slightly higher at between 3.6% - 3.7%. However, with SGOV, you can buy and sell it as you please.

Some alternatives to SGOV include:

WisdomTree Floating Rate Treasury ETF (USFR): Floating-rate Treasuries that adjust with rates. The current SEC 30-day yield is 3.6%.

SPDR Bloomberg 1-3 Month T-Bill ETF (BIL): One of the oldest and most widely used T-bill ETFs. The current SEC 30-day yield is 3.5%.

CLO ETFs (JAAA)

If SGOV is your financial mattress, the Janus Henderson AAA CLO ETF (JAAA) is the mattress with a memory foam topper and maybe a slightly higher chance of mild discomfort. It has a 30-day SEC yield of 4.8% and pays monthly distributions.

JAAA invests in AAA-rated tranches of CLOs (Collateralized Loan Obligations). In plain English, these are bundles of corporate loans sliced into different risk levels. JAAA owns the top-rated slices, which historically have had extremely low default risk. The fund has grown to $26+ billion in assets — a testament to investor appetite for its risk/return profile.

The result: a yield usually around ~5%. So you receive a higher yield than Treasuries, monthly income, and historically low default rates at the AAA level. This is still credit exposure, not government debt. During credit stress, the price can wobble a bit (think 1–3%, not stock-market chaos). Its maximum drawdown since inception was approximately -2.64%, compared to just -0.03% for SGOV.

JAAA is appropriate for investors who understand structured credit and are willing to accept modestly more volatility in exchange for a higher yield. It is not a cash equivalent.

Other alternatives in this category include:

PGIM AAA CLO ETF (PAAA): 4.8% 30 Day SEC Yield

BlackRock AAA CLO ETF (CLOA): 4.86% 30 Day SEC Yield

Panagram AAA CLO ETF (CLOX): 4.81% 30 Day SEC Yield

These funds aim to squeeze a little more income out of fixed income without dramatically increasing volatility.

Conclusion

If you need the money for a house down payment in three months, don’t get cute; stick to VMFXX or a top HYSA. If you are looking to park "dry powder" for a year and want to maximize income while waiting for a stock market dip, a combination of SGOV (for tax efficiency) and JAAA (for the yield boost) is my winning 2026 playbook. Here’s the simplest way I think about it:

Want total safety? Stick with HYSAs and Treasuries

Want flexibility? Use money market funds and SGOV

Want a relatively safe higher income? Add JAAA, corporate, and agency bonds

Want certainty? Lock in rates with CDs or Treasury ladders

That's it for this week! As always, no financial decisions should be made solely on this newsletter, which is for informational and entertainment purposes only and is not intended to be a substitute for advice from a professional financial advisor or qualified expert. If you haven’t already, please subscribe to this newsletter below and never miss an update: