How My Investments Fared In 2024, VOO Investment Update

How my portfolios fared last year

Introduction

With 2025 in full swing (and my therapist on speed dial), it's time to reflect on the market performance for last year. Remember all those doomsday predictions at the start of 2024? Yeah, about that… Turns out, the market decided to throw a party instead of a pity party, delivering returns that made even the most seasoned investors raise an eyebrow (or two).

In this newsletter, I’ll look at how my investments in my equity portfolios fared, and also provide an update on this newsletter’s VOO performance.

Disclaimer: This is NOT financial advice. I am just sharing my strategies, investments, stocks, and index fund strategies, what I'm buying, and where I plan to take those investments. Everyone’s financial goals are different. No financial decisions should be made solely on this newsletter, which is for informational and entertainment purposes only and is not intended to be a substitute for advice from a professional financial advisor or qualified expert.

Also, if you found this newsletter helpful, please share it with one friend who might find it useful by using the button below.

2024 Market Trends

At the beginning of 2024, there was a lot of pessimism in the market. As I noted in the last issue, here are the brilliant forecasts from top analysts for where the S&P 500 would end up:

• JP Morgan: 4,200

• Morgan Stanley: 4,500

• Bank of America: 5,000

• Goldman Sachs: 5,100

• Citi: 5,100

The S&P 500 had a solid year, closing at 5881.63, a 25% gain and a slap in the face to even the most optimistic prediction.

Tech stocks continued their reign of terror (in a good way), with the NASDAQ soaring 29%, thanks to AI and renewable energy – because apparently, we’re all going to be living in the metaverse powered by solar panels. The Dow posted a modest 13% gain, as value stocks outperformed growth stocks in the latter half of the year.

Over the past two years, the Dow has gained 28%, while the S&P 500 has grown 53% and the Nasdaq has grown a whopping 85%.

How My Portfolios Fared

I keep separate brokerage accounts for stocks, retirement, ETF investing (which focuses on dividends but also has funds like VOO and QQQ), fixed income (bonds and CDs), etc. I’ve broken down my positions in each of those accounts in previous newsletters. Here’s a breakdown of how my equity accounts fared (excluding the boring stuff like bonds and real estate):

Stocks at Schwab: This account is focused on individual stocks with the goal of beating the S&P 500. I provided my most recent stock portfolio back in August. Since then, I’ve added Palantir (PLTR) and Boeing (BA). Led by NVIDIA and CAVA, this account returned about 54%, more than double the S&P 500.

ETFs / Index Funds at Fidelity: This account is about that sweet, sweet dividend income, not necessarily beating the S&P 500. It has 16 ETFs / index funds, with 9 focused on dividend income. The last time I posted the funds in this portfolio was last May, and I’ll post an update soon with three ETFs I’ve added since then. For 2024, this portfolio saw a $19.5% gain while providing steady dividend income since I’m morphing into a retiree eyeing early bird specials.

401K at Empower: This is my old 401K account sitting at Empower. This one is simple because the entire account is 1 fund that tracks the S&P 500. The rate of return for 2024 was about 25%, proving that even when I’m not paying attention, my money can still make money.

ROTH IRA at Robinhood: Since I closed my business, I’m back to making annual ROTH contributions by doing a backdoor ROTH IRA conversion, which I wrote about here. In that newsletter, I revealed my simple two-fund portfolio that I use for this account: the Vanguard S&P 500 ETF (VOO) and the Invesco QQQ Trust (QQQM).

Unfortunately, I don’t see a way in Robinhood to get a chart for the performance for 2024, but it’s a little inflated anyway because I moved my account there last April when they had a promotion to offer a 3% match—proof that sometimes, corporate gimmicks actually work. But without the match, the VOO / QQQM combo was up 25% in 2024.

VOO Update

For those new to this newsletter, for a real-world example of dollar-cost-averaging and how I utilize it, I bought the Vanguard S&P 500 ETF (VOO) which tracks the S&P 500 in July of 2022, and have been automatically investing in it every week (I do have VOO in several of our portfolios) while reinvesting the dividends. You can read the details on how much I initially invested and how much I’m adding every week here.

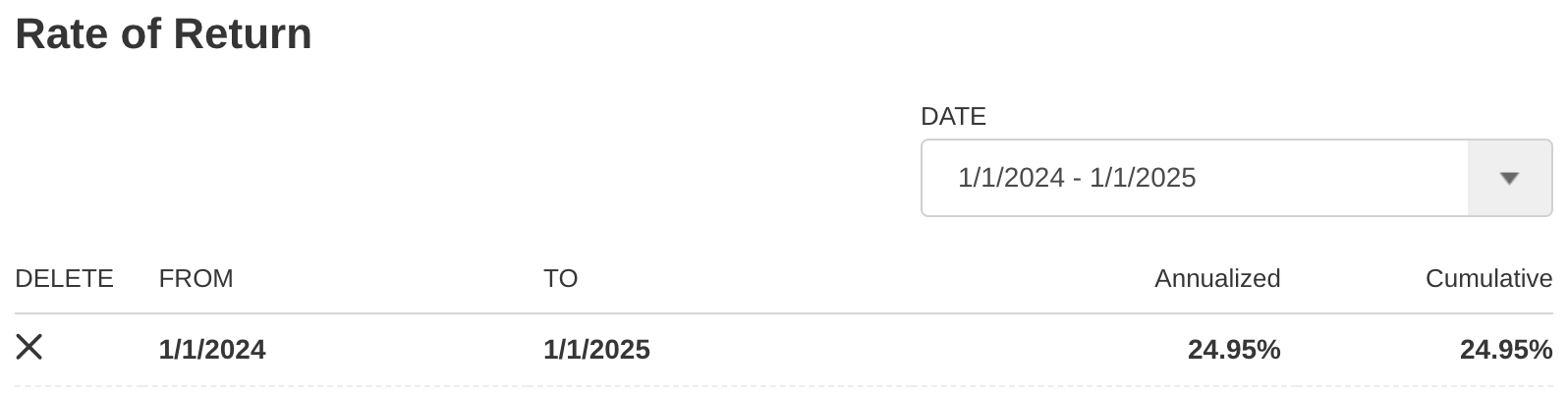

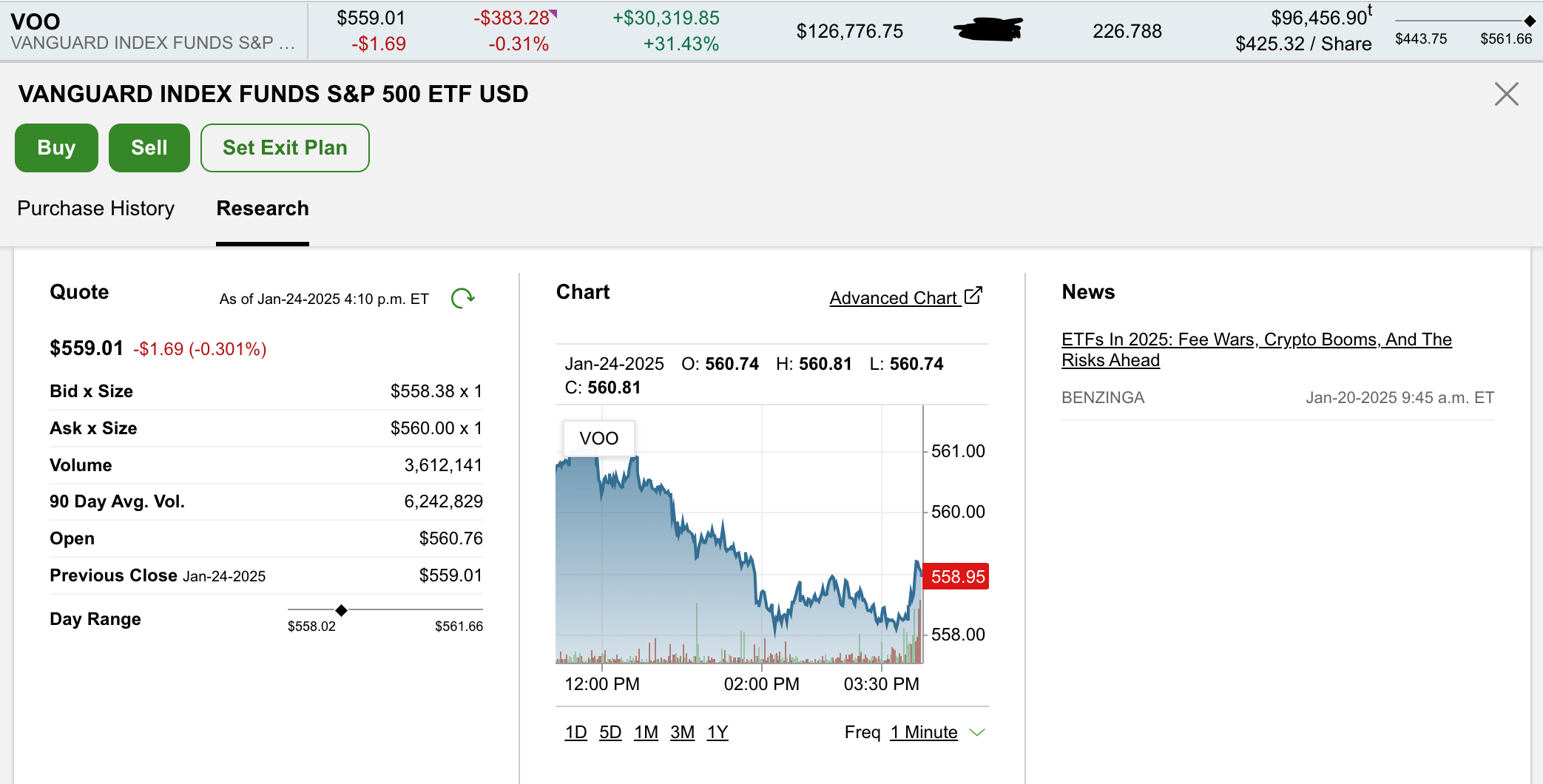

Here is an updated look at how it’s performing after the initial $5000 investment on June 16th, 2002. As seen in the chart below, it has returned about 31% and is up over $30,000, bringing the total value to close to $127,000—a testament to the magic of compound interest and my decision to not panic-sell every time the market sneezed.

Conclusion

2024 was a wild ride. The market defied expectations, my portfolios thrived, and VOO continued to be the responsible adult in the room—but let’s not get too comfortable. The world of investing is a fickle beast, and 2025 could just as easily throw curveballs. While challenges and uncertainties undoubtedly loom on the horizon, I’ll continue to diversify, dollar-cost-average, and try not to lose all my money on meme stocks.

So, here’s to another year of market madness and portfolio growth. If 2025 doesn’t cooperate, well, there’s always lottery tickets—or a career selling inspirational financial quotes on Etsy.

That's it for this week! As always, no financial decisions should be made solely on this newsletter, which is for informational and entertainment purposes only and is not intended to be a substitute for advice from a professional financial advisor or qualified expert. If you haven’t already, please subscribe to this newsletter below and never miss an update: